Introduction: Rebuilding Credit One Step at a Time

Bankruptcy can feel like a financial reset—but it doesn’t mean the end of homeownership or access to credit forever.

Many people are surprised to learn that it is possible to qualify for a second mortgage loan after bankruptcy. However, the process is very different from traditional lending and requires a clear understanding of risks, requirements, and realistic expectations.

This guide explains the basics of second mortgage loans after bankruptcy, how lenders view risk, what borrowers need to qualify, and when this type of loan makes sense.

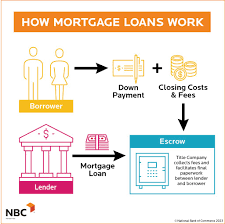

What Is a Second Mortgage Loan?

A second mortgage is a loan taken out against the equity in a property, while a first mortgage is already in place.

Common types include:

- Home equity loans

- HELOCs (Home Equity Lines of Credit)

Second mortgages are considered higher risk because they are repaid after the first mortgage in the event of foreclosure.

How Bankruptcy Affects Mortgage Eligibility

Bankruptcy significantly impacts:

- Credit scores

- Lending history

- Risk assessment by lenders

However, bankruptcy does not permanently block mortgage options.

Common Bankruptcy Types

- Chapter 7: Discharge of unsecured debt

- Chapter 13: Structured repayment plan

Lenders treat these differently when evaluating eligibility.

Waiting Periods After Bankruptcy

Most lenders require a seasoning period before approving a second mortgage.

Typical guidelines include:

- 2–4 years after Chapter 7

- 1–2 years after Chapter 13 discharge or dismissal

These timelines vary depending on lender, loan type, and borrower profile.

Why Second Mortgages Are Harder to Obtain After Bankruptcy

Second mortgages already carry higher risk. When combined with bankruptcy history, lenders face:

- Reduced repayment certainty

- Higher default risk

- Limited recovery options

As a result, borrowers can expect:

- Higher interest rates

- Lower loan-to-value (LTV) limits

- Stricter documentation requirements

Equity Requirements

Equity is critical.

Most lenders require:

- Significant available equity

- Conservative combined loan-to-value (CLTV), often below 80%

The more equity you have, the better your chances of approval.

Credit Rebuilding Is Essential

Before applying, borrowers should focus on:

- Making all payments on time

- Reducing revolving debt

- Avoiding new credit issues

- Establishing post-bankruptcy credit history

Consistent behavior matters more than perfection.

Income and Stability Matter More Than Ever

Lenders look closely at:

- Stable employment

- Reliable income

- Debt-to-income ratios

- Ability to handle higher payments

A strong income profile can offset past credit challenges.

Interest Rates and Loan Terms

Borrowers should expect:

- Higher interest rates than standard loans

- Shorter repayment terms

- Potential balloon payments

Understanding the full cost of borrowing is critical.

Acceptable Uses for a Second Mortgage After Bankruptcy

Lenders are more comfortable when funds are used for:

- Home improvements

- Debt consolidation

- Emergency expenses

- Necessary repairs

Using equity responsibly improves approval odds.

Risks You Must Understand

Second mortgages after bankruptcy carry real risk:

- Higher monthly payments

- Reduced financial flexibility

- Potential foreclosure if payments are missed

Borrowers must ensure the loan strengthens—not weakens—their financial position.

Alternatives to Consider

Before committing to a second mortgage, consider:

- HELOCs with flexible draws

- Personal loans

- Waiting longer to rebuild credit

- Budget restructuring

Sometimes patience is the smartest strategy.

When a Second Mortgage Makes Sense After Bankruptcy

A second mortgage may be appropriate when:

- Credit has been rebuilt responsibly

- Equity is strong

- Income is stable

- Funds serve a productive purpose

This is a strategic tool—not a quick fix.

Key Questions to Ask Before Applying

- How long since bankruptcy discharge?

- What is my available equity?

- Can I afford higher payments?

- What happens if my income changes?

- Are there prepayment penalties?

Clear answers reduce future stress.

Common Mistakes to Avoid

- Borrowing too soon

- Ignoring total loan cost

- Overleveraging home equity

- Assuming refinancing will be easy later

Caution and planning matter.

Conclusion: Knowledge Is the First Step Forward

Qualifying for a second mortgage loan after bankruptcy is possible—but it requires preparation, discipline, and realistic expectations.

This type of loan should support long-term recovery, not recreate past financial stress. When approached thoughtfully, it can be a useful tool in rebuilding financial stability.

The key is understanding the basics, knowing your numbers, and choosing progress over urgency.

Word Count:

401

Summary:

Getting a 2nd mortgage loan or home equity loan after a bankruptcy is workable. However, loan applicants should be aware of certain disadvantages to bad credit loans. A bankruptcy is destructive to credit scores.

In reality, many financial experts discourage bankruptcies. Those who file Chapter 7 or Chapter 13 are subjected to higher finance rates on homes, cars, etc. Before applying for a 2nd mortgage, know what to expect and understand the basics of getting a reasonable …

Keywords:

2nd mortgage, home equity loan, bankruptcy

Article Body:

Getting a 2nd mortgage loan or home equity loan after a bankruptcy is workable. However, loan applicants should be aware of certain disadvantages to bad credit loans. A bankruptcy is destructive to credit scores.

In reality, many financial experts discourage bankruptcies. Those who file Chapter 7 or Chapter 13 are subjected to higher finance rates on homes, cars, etc. Before applying for a 2nd mortgage, know what to expect and understand the basics of getting a reasonable rate.

Expect Higher Finance Fees or Interest Rates

After a bankruptcy, many people are hesitant to apply for credit. They expect higher rates, which will also increase monthly payments. However, obtaining new credit accounts is crucial to re-establishing and building credit history. On the other hand, getting a lender to approve a credit card application after a bankruptcy is challenging. For this matter, some people choose to get a 2nd mortgage loan.

Getting approved for a 2nd mortgage following a bankruptcy is easier because the loan is secured by your home or property. Thus, if you stop paying on the loan, the lender may claim your property and resell it to recoup their loss.

While these loans are great for improving credit, applicants should not expect the best rates. Traditionally, 2nd mortgage loans have higher rates than first mortgages. However, if you have a recent bankruptcy, anticipate above average rates. To avoid a huge monthly payment, borrow a small amount of money.

Another option involves borrowing money, and depositing the funds into a savings account. Over the course of six months, repay the lender using the deposited funds. This way, you improve credit history and avoid the risk of not being able to repay the loan.

Using Sub Prime Loan Lenders For Best Rates

Applying for a 2nd mortgage with your current lender may not be the best option. If you obtained your first mortgage with good credit, the lender may not approve your loan application following a bankruptcy. Instead, contact several sub prime lenders. Sub prime lenders approve loans for all credit types. Hence, applicants can get approved after a bankruptcy, foreclosure, repossession, etc.

Furthermore, sub prime lenders usually offer better rates than traditional mortgage lenders or banks. Online mortgage brokers can help you find a bad credit or sub prime lender. Moreover, brokers offer applicants various loan options. As a result, loan applicants can select the lender offering the best rate and loan terms.

Tinggalkan Balasan